For the week of July 13th

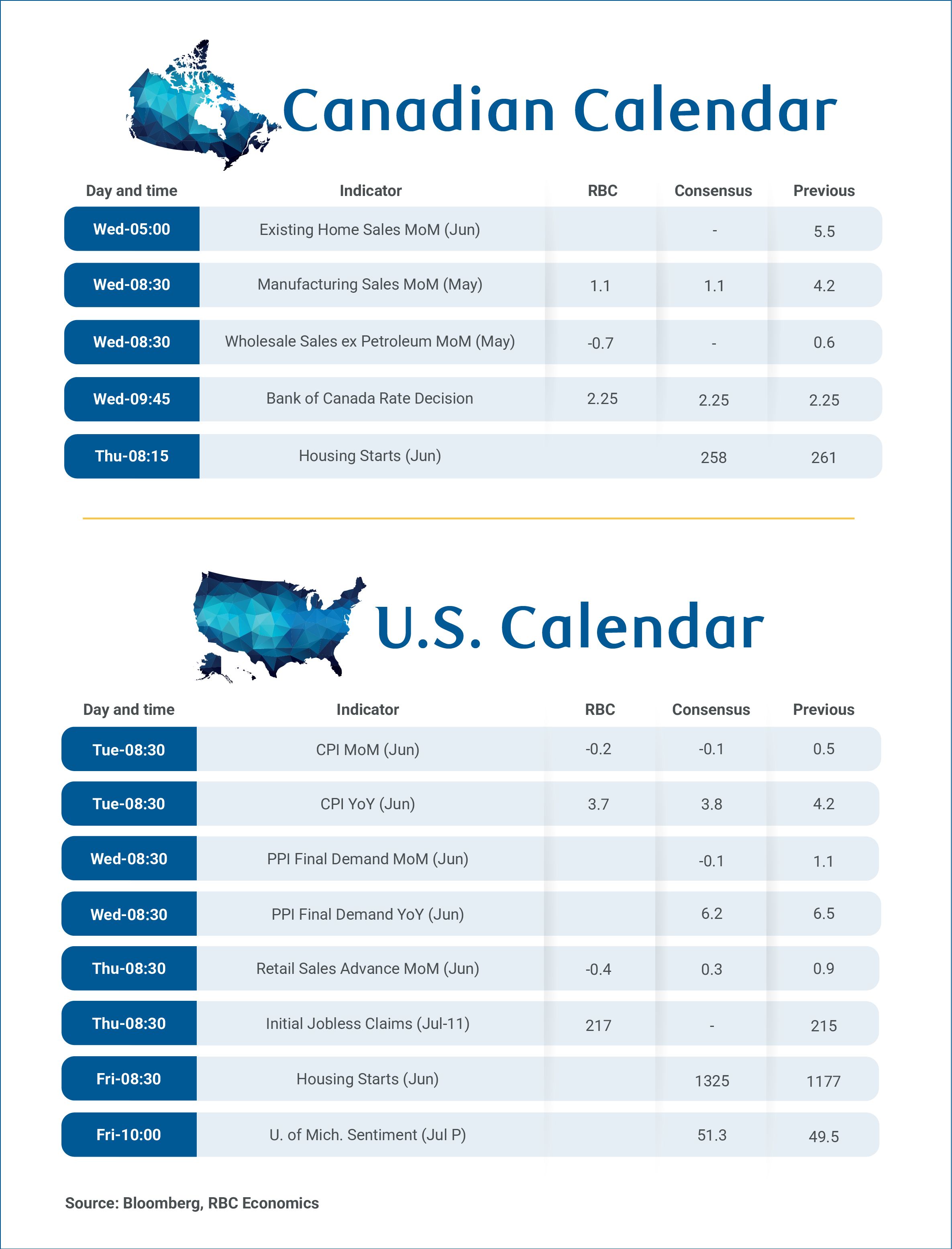

The Bank of Canada is widely expected to hold the overnight rate at 2.25% at Wednesday’s policy announcement—marking a sixth consecutive pause after 50 basis points of cuts over September and October last year.

The BoC highlighted two-sided risks to the interest rate in their prior policy meetings – risks of cuts tied to potential downside growth surprises and hike risks due to concerns that higher energy prices from conflict in the Middle East could lead to “generalized inflation.”

But both concerns have broadly eased over the last month to help solidify expectations for the central bank to remain in a wait and see mode for now.

The spike in oil prices has yet to show significant signs of turning into a broader longer-lasting inflation shock. Higher gasoline prices have raised costs for households, but price increases haven’t generally spread across the consumer spending basket. The BoC’s Business Outlook Survey showed businesses’ longer-run inflation expectations still well-anchored in May when oil prices were at recent peaks. And oil prices have since moved lower despite still significantly restricted traffic through the Strait of Hormuz.

At the same time, Canada’s growth and labour market data have looked better after a downside surprise in Q1 gross domestic product growth.

Critically, CUSMA continues to protect the bulk of Canadian exports from U.S. tariffs despite the U.S. administration opting not to (yet) extend the 2036 expiry date of the deal, and broader U.S. tariff rates have been edging lower.

Monthly GDP data so far is pointing to stronger growth in Q2. Labour markets showed more signs of steadying in May and June after job losses earlier in the year. Our tracking of consumer spending has remained resilient. And housing markets have firmed in cities like Toronto and Vancouver that significantly underperformed previously.

We’re also looking ahead to May’s manufacturing and wholesales’ reports on Wednesday. Both should look softer than in April, particularly controlling for higher energy prices, but not enough to retrace larger gains in the prior months. Statistics Canada’s advance estimate is for a 0.1% increase in real GDP in May after a 0.5% April increase, leaving growth in Q2 tracking in line with an about 2% annualized rebound.

Overall, we continue to expect a soft but gradually improving Canadian per-person growth backdrop will leave the BoC on hold through 2026.

-

U.S. CPI growth likely remained elevated but slowed in June with gasoline prices falling ~10% (on a seasonally adjusted) basis from May. We look for headline CPI growth to edged down to 3.7% after rising above 4% for the first time in three years in May. Excluding food & energy products, we expect core inflation to remain elevated at 2.8% on a 0.2% month-over-month increase.

-

We expect U.S. retail sales edged down 0.4% in June driven by a sharp pullback in oil prices lowering spending at gasoline stations. Accounting for price changes, spending should still look firm, supported by a 2.8% increase in unit vehicle sales and an assumed 0.4% increase in control (excluding gasoline stations, motor vehicle sales, and building material stores).

About the authors:

Nathan Janzen is an Assistant Chief Economist, leading the macroeconomic analysis group. His focus is on analysis and forecasting macroeconomic developments in Canada and the United States.

Claire Fan is a Senior Economist at RBC. She focuses on macroeconomic analysis and is responsible for projecting key indicators including GDP, employment and inflation for Canada and the US.

Explore the latest from RBC Economics:

Podcast: The 10-Minute Take. Where could CUSMA Joint Review go from here?

Q2 Business Outlook Survey: Surprisingly robust sentiment amid oil shock

Canadian trade surplus widened further in May

Canada’s unemployment rate edged lower in June

Canada’s housing markets hit some bumps in June

June spending holds steady as Canadians balance essentials and experiences

Share these insights with your network:

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.