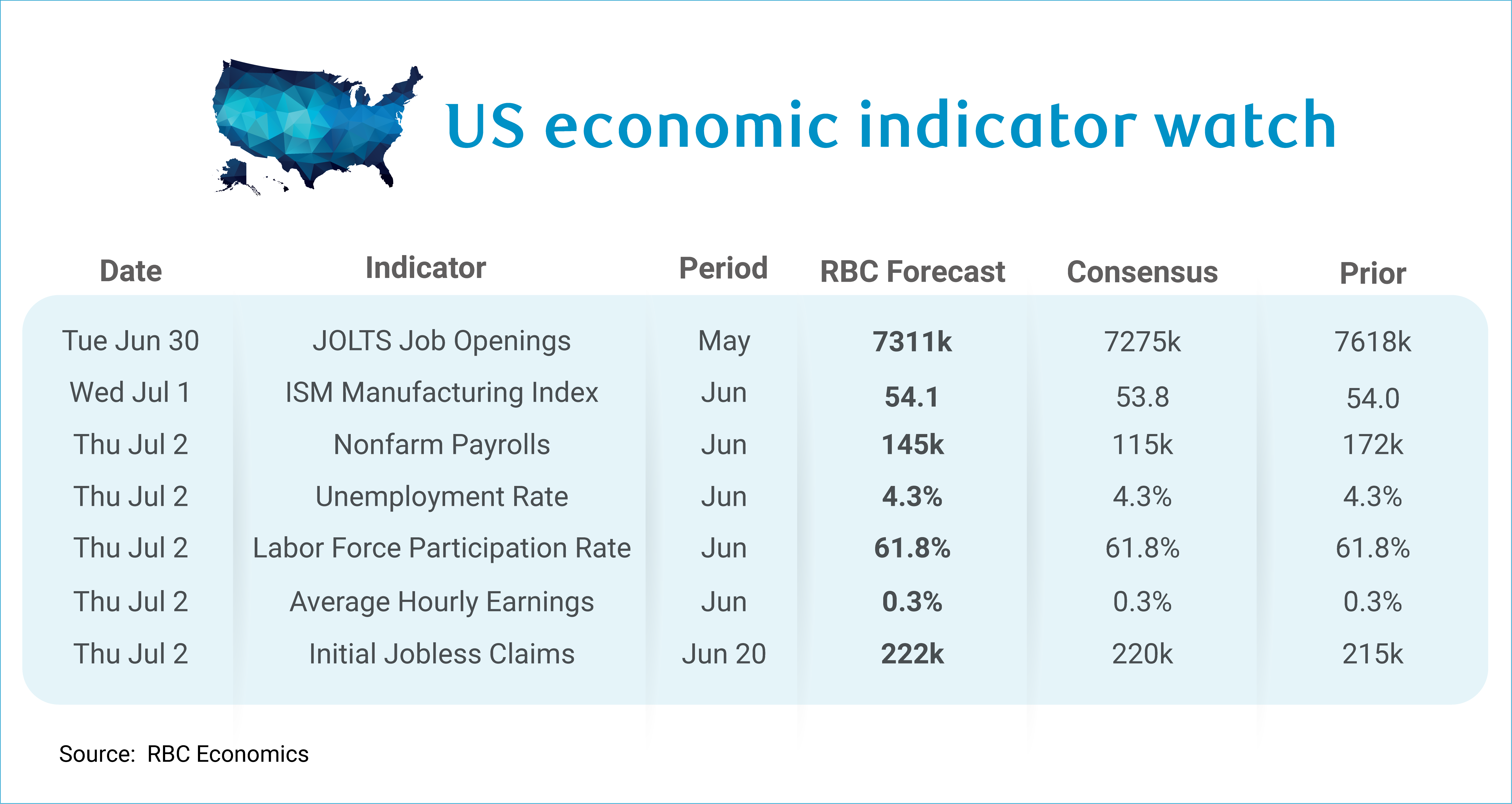

Next week, all eyes will be on the June jobs report — though for a Fed laser-focused on inflation, we expect the June data will continue to provide reassurance rather than cause for concern from a Fed that largely treated the labor side of the mandate as an afterthought at the June meeting. We expect +145K jobs were added in June with the unemployment rate holding steady at 4.3%.

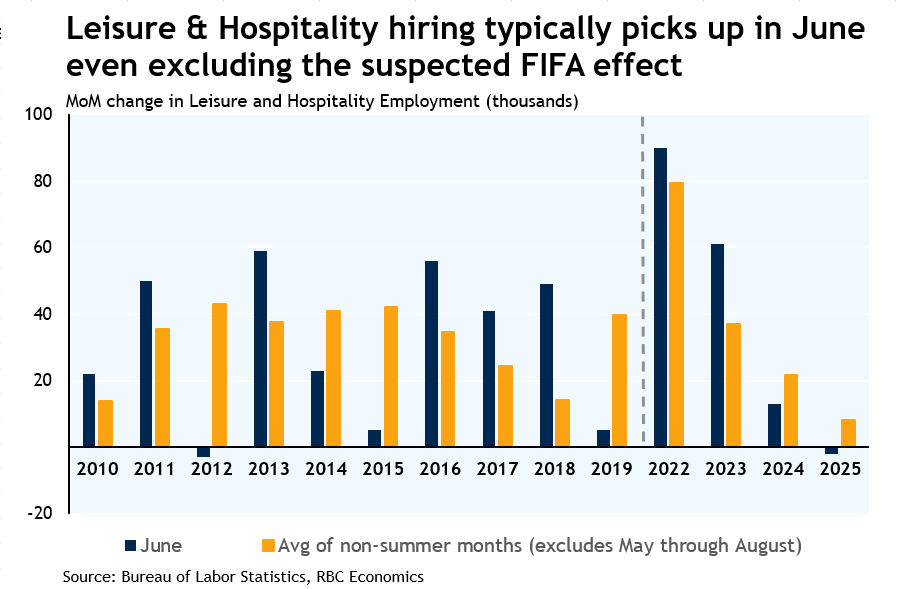

The nonfarm payrolls prints in 2026 look different than 2025. Nearly +570K jobs have been added so far this year (averaging +114K per month), compared to a paltry +116K in all of last year. June should continue this streak, with an added tailwind: the World Cup. Leisure and hospitality added +70K in May — mostly food services and drinking places — and we expect hiring held steady in June as stadiums, bars, and restaurants staffed up. We’d reasonably expect these gains to reverse by August once the tournament wraps.

But the strength isn’t just a World Cup story. Even outside of leisure and hospitality, monthly hiring has consistently exceeded +100K. Health care still accounts for the lion’s share, but the composition is broadening. Trade-exposed sectors like manufacturing and transportation and warehousing are adding back jobs shed in 2025. The weak spots remain concentrated in white-collar industries — information, commercial banking, and real estate — which continue to shed positions.

One wrinkle: we expect an influx of new labor market entrants in June as the school year ends, and college students search for summer jobs. This is seasonal and typical, but it adds bodies to the labor force and works to offset retirements. All else equal, we expect the participation rate will hold steady (at 61.8%) in June.

Here’s what else we’re watching next week:

-

JOLTS data for May is stale, but we expect to see fewer job openings (+7311k) relative to the prior month. Indeed job postings data showed a retracement in May. The JOLTS job openings rate is in line with pre-COVID levels, but hire rates, on the other hand, remain exceptionally low. This suggests that firms are quicker to post positions than they are to fill them. This is unsurprising given the fact that the unemployment rate for those under 25 remains elevated even though prime-age unemployment remains low.

-

We don’t expect to see much movement in the ISM manufacturing Index in June. Most regional Fed manufacturing indexes improved (Philly and Kansas City) or held steady (Texas). Both Richmond Fed and Empire State Surveys weakened slightly.

-

Average hourly earnings likely continued to rise +0.3% m/m in June which will keep the year-over-year pace of earnings growth elevated. But wage growth is roughly in line with core PCE and well below headline PCE—earnings are not keeping up with inflation.

-

Initial jobless claims will likely come in slightly firmer for the week ending June 20th (we expect +222k).

About the authors:

Mike Reid is Head of US Economics at RBC. He is responsible for generating RBC’s US economic outlook, providing commentary on macro indicators, and producing written analysis around the economic backdrop.

Carrie Freestone is a Senior US Economist at RBC. She is responsible for generating RBC’s US economic forecasts across GDP, employment, and inflation, and providing macro commentary through publications, presentations, and the media.

Imri Haggin is an US Economist at RBC, where he focuses on thematic research. His prior work has centered on consumer credit dynamics and treasury modeling, with an emphasis on leveraging data to understand behavior.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. The reader is solely liable for any use of the information contained in this document and Royal Bank of Canada (“RBC”) nor any of its affiliates nor any of their respective directors, officers, employees or agents shall be held responsible for any direct or indirect damages arising from the use of this document by the reader. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

This document may contain forward-looking statements within the meaning of certain securities laws, which are subject to RBC’s caution regarding forward-looking statements. ESG (including climate) metrics, data and other information contained on this website are or may be based on assumptions, estimates and judgements. For cautionary statements relating to the information on this website, refer to the “Caution regarding forward-looking statements” and the “Important notice regarding this document” sections in our latest climate report or sustainability report, available at: https://www.rbc.com/community-social-impact/reporting-performance/index.html. Except as required by law, none of RBC nor any of its affiliates undertake to update any information in this document.